Or to put it less succinctly — pros (the good ones) apply a process, amateurs follow the crowd.

* Credit for the title goes to Christopher Schelling. You will see he clearly falls in the ‘former’ category.

Thankfully, some of the leading venture firms (see HERE, HERE & HERE) are starting to migrate their venture funds and firm strategies to look more like portfolio managers and less like deal junkies.

Simultaneously, the tourist investors are running for the hills…in the public markets as well as venture investors.

Liquidity = FOMO

Sadly, there is an entire generation of ‘investors’ in both the public and private markets — conditioned by the flood of liquidity — to ‘Buy High, Sell Higher’.

As a ‘pragmatic Libertarian’ I’m a firm believer in caveat emptor. The Robinhood/crypto/NFT crowd can gamble away their money all they want.

But when that same audience represents a meaningful proportion and the dominant narrative of how we fund innovation, I feel compelled to dust off ‘Buffett-isms and subject myself to the youthfully disdainful (and predictable) ‘you just don’t get it’ reactions.

Buffett-ism #1:

Be greedy when others are fearful, and be fearful when others are greedy.

I’m guessing this was his way of explaining Buy Low/Sell High, but I could be wrong.

What I’m pretty certain of is that the majority of investors in early stage startups base their buying decisions based on ‘the crowd’. And that crowd is largely made up of FOMO investors; Buy High/(hopefully) Sell Higher.

Well, that sound you hear are the FOMO investors (both public and private) sounding the horns of retreat.

Asset Class vs ‘Access’ Class

Innovation is finally coming to the very process we fund innovation. Sequoia’s announcement last fall has forced forward thinking vcs (or just those that want to be part of the future of venture capital) to finally recognize (and maybe read) the BODY of RESEARCH which defines an optimized venture fund strategy to manage all risks properly, so institutional investors can approach early stage investing as an asset class vs. an access class:

- Non-systematic Risk; also known as company or transaction risk. This is NOT solved via more due diligence (or relying on the work of others). Diversification is the only way to manage non-systematic risk properly.

- Systematic Risk; also known as market or timing risk. Dollar cost averaging (think Scout/Opportunity Fund strategy) is the only way to manage systematic risk.

- Decision-Process Risk; also known as Behavioral Finance. Think what ‘MoneyBall’ did for sports to eliminate the biases in decision making. As Nobel Laureate Daniel Kahneman said — ‘Algorithms beat human bias, and simple algorithms beat complex ones.’

Institutionalization of Venture

Notwithstanding the recent activities and track records of Softbank & Tiger Global, institutional capital will continue to flow to venture capital — particularly the earlier stages.

But to accommodate the $Trillions that will be migrating away from public securities and into the private markets seeking higher nominal alpha, the venture industry (apprenticeship guild, really) needs to become more professionalized. Processes and systems (see recommended systems tech stack) will become more relevant due diligence criteria for LPs/investors. Maybe there will even be a proper training/certification — a ‘Certified Venture Investor’ curriculum and accreditation process established soon.

And as the big asset management platforms accelerate their entry into early stage investing, those small/emerging managers (and/or their investors) that rely on the old narrative (‘we’ve got access to quality deal flow’, ‘we know what a good deal looks like’, ‘we add value and are entrepreneur-friendly’) will look like the ‘dumb money’.

The Future of Venture Capital — More Antifragile

The industry is finally innovating. Professionalism is happening. And none too soon.

This future was well explained in the research report on the venture industry, funded by a Singapore investor and conducted by Innosight, the consulting firm founded by Clayton Christensen — The Future of Venture Capital.

We need a more ‘antifragile’ funding ecosystem for worthy startups all over the country. We can’t keep going through the boom/bust cycles, benefiting a few people & regions around the country, while excusing away the destruction of $B’s of risk capital with the excuse — ‘I guess we got carried away, so now is the time for startups to tighten their belt.’

In other words, we need more venture ‘pros’….

But whatever you do, read and internalize The Future of Venture Capital report — if you want to be part of that future.

Portfolio Managers Defining the Future of Venture Capital

The migration of Sequoia, Bessemer, a16z, and General Atlantic before that, to become Registered Investment Advisors, signals the industry is finally evolving.

As The Future of Venture Capital report linked above suggests, many venture funds of the future will look more like mutual funds or ETFs than the conventional fund model, which were more of a collection of individual transactions assimilated into a fund structure, with investment decisions driven by a transactional focus.

The upcoming Fall Edition of Institutional Investors Journal of Portfolio Management will be focusing on the venture and PE industries, with articles already on their website defining what those institutionally rigorous venture portfolios might look like, and why:

- Better risk management via proper diversification, proper staged capital deployment, data-driven decision models, optimal ‘decision process risk’ management (what Lightspeed Ventures acknowledged they finally implemented processes to address)

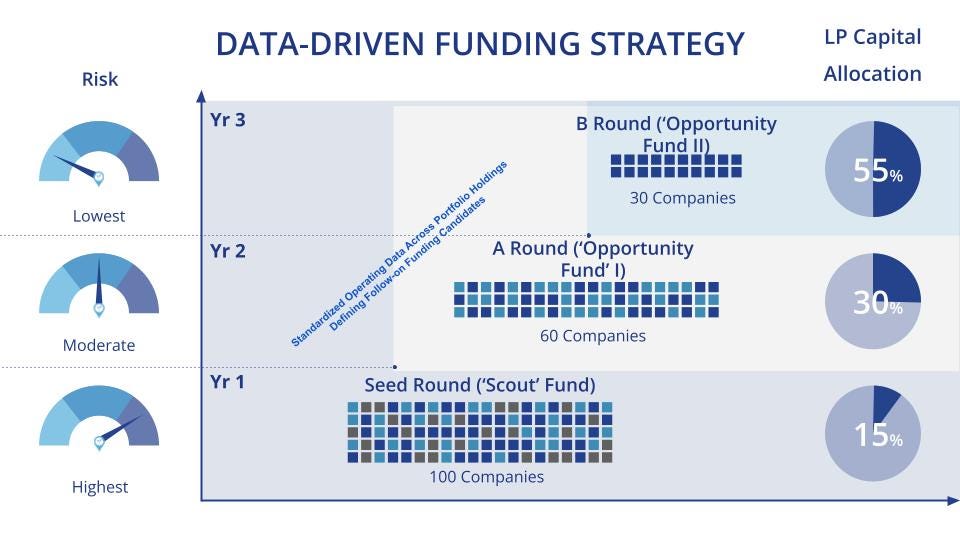

An optimized venture fund strategy will look something like the illustration below:

For a ‘Seed to B’ round venture strategy where LPs are taxable, a further optimization strategy would be to incorporate the Qualified Small Business Stock tax incentives; QSBS Sec. 1244, QSBS Sec. 1202 (and 1045 exchange opportunities):

These laws have been around since 1958 for Sec. 1244, and 1993 for Sec. 1202.

The power and importance of focusing on after-tax implications is brought to proper relief below, when viewing a sample $1M fund return profile, one optimizing on after-tax returns, the other not:

Assumptions: All portfolio holdings were QSBS qualified, all LPs were taxable, failed startups were written off against ordinary income (Sec. 1244), and all gains were in companies that were held past the required 5 year holding period to utilize Sec. 1202.

By simply utilizing existing tax incentives, LPs in a tax-optimized (QSBS Fund) would increase the returns for LPs in dollar terms by 28%.

A larger question is why venture funds that invest across the Seed to B rounds haven’t been doing this before?

Conclusion

The venture industry was informally launched in 1948, but really took off since the first GP-led venture partnership was launched in 1959.

It as taken over 60 years, but with the changes by Sequoia, et. al., now in full swing, it appears the industry is finally evolving from a guild/apprenticeship model to a more professional investment management industry.

For all those investors over the past 60 yrs that didn’t properly profit from your venture investments, the industry should be sorry. What was gambling was sold to you as investing.

For those that have waited patiently on the sidelines, your ‘Buffett moment’ to get greedy in the venture asset class is coming.

Note on the author:

I was a professional RIA for over 20 years managing a multi-family office. We did our own securities research and built portfolios for HNW individuals. While we built portfolios with individual stocks, we didn’t view ourselves as stock pickers (deal junkies). We were portfolio managers in the Large Cap Core style box, with a GARP (Growth At a Reasonable Price) flavor of stock.

From 3/31/1996 through 3/31/2009 we were recognized by multiple 3rd party databases as the #1 best performing Large Cap Core manager, in both absolute and risk-adjusted terms, after fees.

https://joe-26467.medium.com/pros-construct-portfolios-amateurs-chase-deals-3d0dd8f43ddc