Or, what if Danny Kahneman & Annie Duke walked into a bar….

….and decided to design a better venture funding process?

What if …Steve Case is right — that not only is there an opportunity gap in this country, but there are many worthy entrepreneurial efforts across the country getting overlooked?

What if…the concentration of venture activity on the coasts is, in fact, unhealthy for our country?

What if… the opportunity gap caused by the lack of risk capital is the same opportunity gap that is fueling the opioid epidemic? Or the acceleration in suicide rates?

How would you mobilize more capital into more regions in the country quick enough to slow the despair felt by so many young people, and possibly give them hope?

How would you invest the capital that would give an effective risk-adjusted return for the investors?

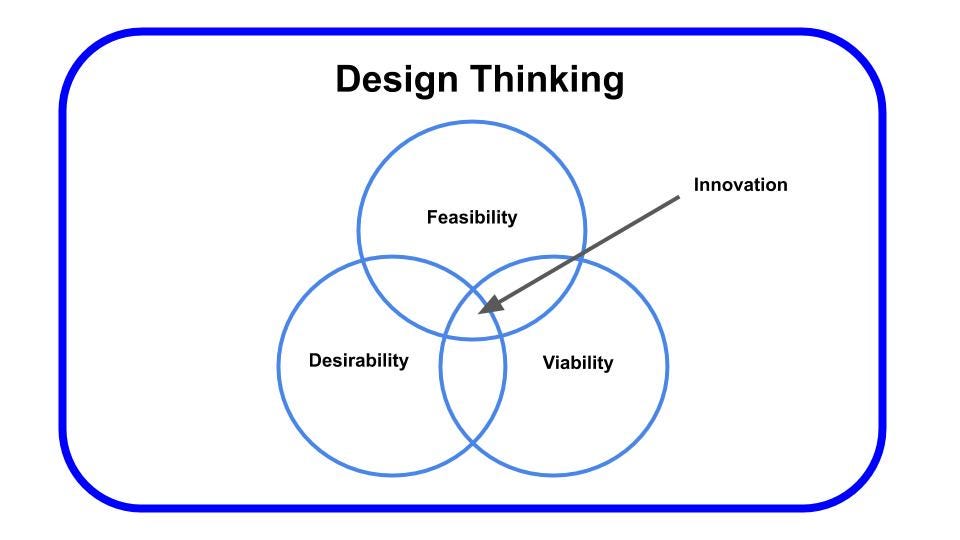

Using Design Thinking to Unpack and Solve the Problem — “We can not solve our problems with the same level of thinking that created them” Albert Einstein

What are the elements of Design Thinking?

According to Wikipedia, the core features of Design Thinking include abilities to:

- Resolve ill-defined or wicked problems

- Adopt solution-focused strategies

- Use adaptive/productive reasoning

- Employ non-verbal, graphic/spatial media

Wicked Problem

There is clearly a funding and opportunity gap in the U.S.

When 80+% of venture dollars are concentrated in 4 regions; NY, Boston, Silicon Valley/SF and LA, getting more startups funded across the country represents is a wicked problem.

This concentration of investing has not resulted in good outcomes for the investors in venture funds. Investors have also not enjoyed a return commensurate with the risks they take, as LPs (relative to VCs) in venture funds, as reflected in this Harvard Business Review article:

Angels don’t fare any better, as is to be expected. According to Robert Wiltbank of the Willamette University, if angels diversified properly, they could receive an appropriate risk-adjusted return. But how many angels have portfolios of 100+ startups?

Adopt Solution-Focused Strategies

If the wicked problems are;

#1 — Not enough startups get funded across the country

#2 — Investors don’t get compensated properly

It would seem the ‘Solution-focused Strategies’ should result in:

- Worthy startups seeking capital would receive funding, regardless of their location

- Investors would be compensated for their investment of time and capital

Both Desirable outcomes indeed consistent with Design Thinking (see Venn Diagram above).

The question is how…

Adaptive/Productive Reasoning

If the traditional model of concentrated portfolios formed and funded in the 4 regions mentioned above represents what needs design thinking to fix, then:

- Diversified portfolios spread across the country would be a logical goal.

Two of the principal contributing factors of the chronic underperformance of portfolios — in both public securities as well as venture portfolios — are high fees and the ‘stock-picker’s fallacy’, then:

- Any funds should involve low(er) fees and proper (i.e., ‘index fund-like) diversification — with minimal human influence/bias in who gets funding.

In fact, research is available confirming proper diversification does capture the asymmetric return potential of the venture asset class while managing the non-systematic (company specific) risks that concentrated portfolios don’t.

Again, the question is how…

Design Thinking

- Wicked Problem — How do assemble ‘index fund-like’ venture portfolios across the country?

- Solution-Focused Strategy — Don’t ‘re-create the wheel’. Look to where ‘index fund-like’ portfolios have been assembled elsewhere.

Index funds are readily available to investors across the country, to invest in companies across the country. Go to Vanguard, State Street, BlackRock or Dimensional Fund Advisors. They do it every day — in the public markets — whether they are open ended mutual funds, closed ended ETFs or Unit Investment Trusts.

How were they assembled?

The ’33 and ‘40 Act(s)’ Made It Possible

The Securities Act of 1933 (’33 Act) established the rules and regulations to lessen the risks of investing in publicly traded securities in response to the Market Crash of 1929.

- The ’33 Act is based upon a philosophy of disclosure, meaning that the goal of the law is to require issuers to fully disclose all material information that a reasonable shareholder would require in order to make up his or her mind about the potential investment.

The key is the spirit of disclosure — reporting requirements placed on companies that wanted to be publicly traded and thus have access to a wider audience of investors.

Solution-focused Strategy #1 — Require reporting/disclosure from companies seeking capital.

The ’40 Act outlined additional instruments — funds as outlined above — which could help investors manage the risks (through diversified ’40 Act funds) of investing in publicly traded stocks.

Solution-focused Strategy #2 — Invest in diversified, ’40 Act-like’ products.

Given the lack of standardized accounting, reporting requirements and public markets to research and trade private companies, efficiently assembling a diversified portfolio is pragmatically impossible — currently.

There is good work being done to create a secondary market for private securities.

And while Title III of the JOBS Act requires annual reports as a first step in introducing reporting requirements for private companies, to date there is no standardized reporting or transparency requirements on Reg D offerings.

That’s not to say investors can’t — or shouldn’t — require some level of consistent reporting.

In fact, research confirms what many investors have already experienced — those startups where the CEO is voluntarily transparent dominate the universe of successful startups. And the opposite is true — the single most consistent character trait (read due diligence) of the universe of failed startups is the absence of transparency.

Theranos anyone?

Adaptive/productive Reasoning #1 — Investors should require it BEFORE they invest.

Adaptive/productive Reasoning #2 — Investors should invest in diversified ’40 Act — like portfolios that require evidence of transparency BEFORE the fund invests.

But again, how?

How are properly diversified portfolios assembled with little human intervention?

The Public Markets Offer a Solution

There is a growing recognition that even the most successful venture capitalists accept luck plays a large part in delivering out-sized returns (HERE and HERE).

But ‘hope and luck’ is not a sufficient portfolio assembly strategy. Nor is it scalable.

The answer is through filtering vs. security selection.

Dimensional Fund Advisors has built a very nice business creating index-like portfolios that have performed well relative to benchmarks using a Smart Beta filtering strategy.

Factors or character traits of the companies YOU DON’T WANT are researched and defined ahead of time, then the universe of candidates is compared to those factors, and those that DON’T qualify are filtered out.

What is left is a diversified portfolio of companies which have the character traits you want, within an asset class of your choosing.

Why shouldn’t the same be done with startups?

Adaptive/productive Reasoning #3 — Assemble a properly diversified (100 to 200 companies), index fund-like (equal weighted) portfolio using a Smart Beta filtering process.

Filters should be selected based on their de-risking character traits, not on an assumption that it will isolate ‘hot deals’. This is the slippery slope of bias that inflicts the many under-performing venture funds today.

The filters would act like an algorithm, which reinforces objectivity, and is scalable.

It so happens that this strategy is supported by a Nobel Prize (in Economics) winning psychologist, whose work is the basis of the ‘Money Ball’ movement — Daniel Kahneman.

How to Scale Across Geographies

If one were to assemble a solution for a specific need (better fast food menu, car servicing, niche lodging provider, etc.) there are a few ways to replicate and scale that (branded?) solution across a wide geography.

Raise a BUNCH of capital and do it yourself (with all the commensurate execution and financial risk), or franchise the playbook.

If speed is also a goal, then franchising would likely represent the most efficient path.

Adaptive/productive Reasoning #4 — Assemble a franchise-able model or platform that could assemble properly diversified (100 to 200 companies), index fund-like (equal weighted) portfolio using a Smart Beta filtering process across a wide geographic footprint.

Seems quite Feasible when the public markets’ practices provide such tangible examples of what to do and what not to do.

Conclusion

When reviewing the illustration above:

Clearly this would be a Desirable outcome if such a model or platform were available.

It would logically seem Feasible, given the examples and existing practices in the public markets proffered above.

But is it Viable?

Clearly this has not been done before. Otherwise we wouldn’t still have the wicked problems discussed above.

Until now…

In fact, it was profile in an international publication — the Family Wealth Report.

There is finally some innovation coming to the very funding mechanism and process that has funded innovation in multiple industries.

And Danny and Annie will be proud to see their good work put to good use….

https://joe-26467.medium.com/what-if-steve-case-is-right-b881a8c6ac5c